Fool’s Gold – Innovation, Ignorance, and the Price We Paid

Let’s Decode the Words First

Finance is full of jargon. Most of it exists not to explain—but to confuse. Before diving into Fool’s Gold, here’s a short dictionary to help make sense of what’s intentionally made complicated:

CDS (Credit Default Swap): A kind of insurance on a loan—if the borrower defaults, someone else pays the loss.

CDO (Collateralized Debt Obligation): A bundle of loans sold to investors. Risky inside, but labeled “safe.”

CDO-squared: A bundle of CDOs made from other CDOs. Risk layered on top of risk.

Gaussian Copula: A formula used to calculate how likely different loans are to fail together. It worked perfectly—until reality hit.

Bailout: When governments use public money to rescue failing companies.

Subprime Loan: A loan given to someone with low credit or low income—high chance of default.

Leverage: Using borrowed money to invest more. Increases both gains and losses.

Finance isn’t complex because it has to be. It’s complex so people stop asking questions.

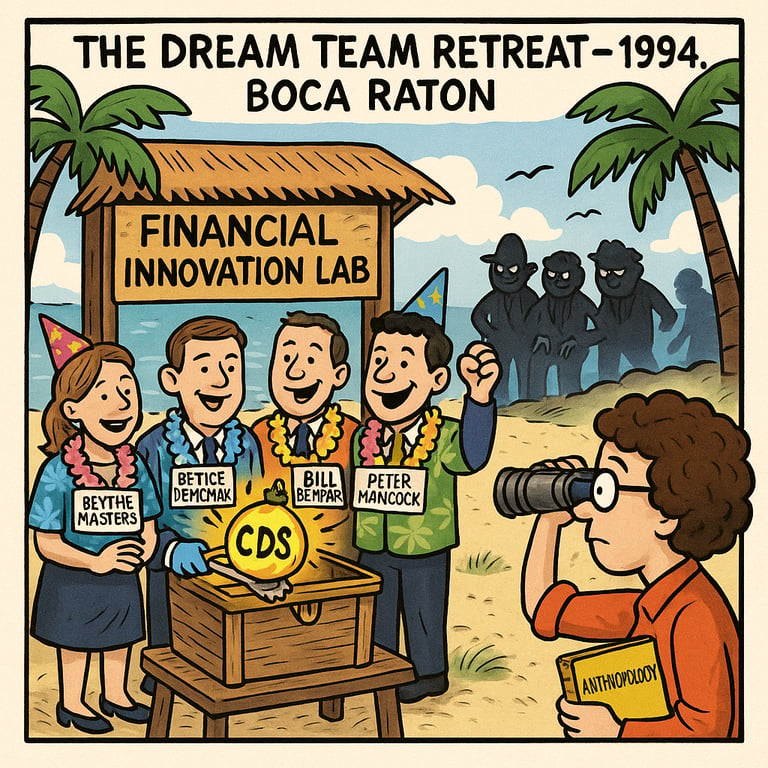

The Story Begins – Gillian Tett & the Dream Team

Fool’s Gold is written by Gillian Tett, a journalist at the Financial Times with a PhD in anthropology. That background matters—because while everyone else watched the money, she watched the behavior.

In 1994, JPMorgan sent a group of bright young bankers to a retreat in Boca Raton, Florida. Known as the “Dream Team,” they included Blythe Masters, Bill Demchak, Peter Hancock, and Andrew Feldstein. Their goal: reduce the bank’s credit exposure without selling loans.

Their solution? The credit default swap (CDS)—a way to transfer risk like passing a hot potato. It was innovative. It was efficient. It worked.

And then, everyone else got involved.

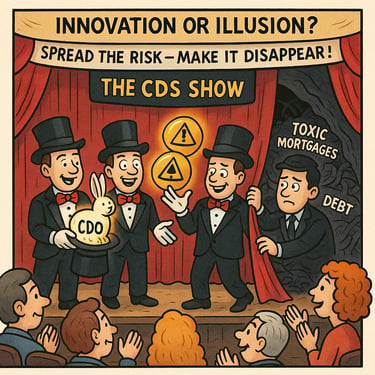

Innovation or Illusion?

Wall Street embraced CDS like a golden ticket. Soon, banks began building CDOs, bundling risky mortgages and selling them as safe investments. Then came CDO-squareds—CDOs made out of other CDOs. It was complexity layered on complexity.

The logic was simple: spread the risk wide enough, and no one gets hurt.

Except that wasn’t true. The risks weren’t gone—they were just hidden.

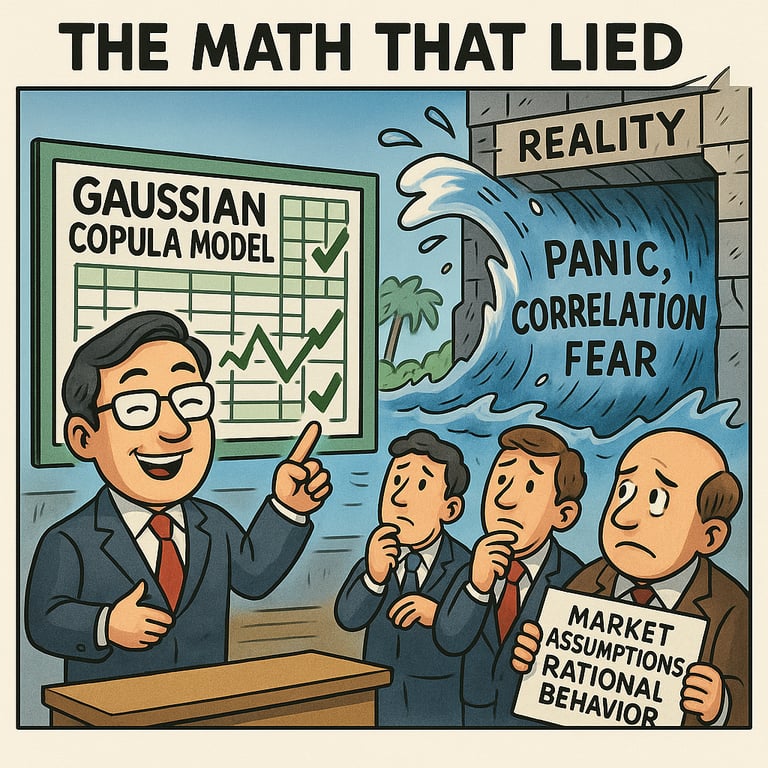

The Math That Lied

To justify it all, banks used a formula called the Gaussian copula. It estimated how likely it was that multiple loans would fail at the same time.

It was clean, quick, and dangerously misleading.

It assumed markets behaved rationally.

It ignored fear, panic, and correlation.

It worked great in Excel. It failed in reality.

The model made people feel safe—right up until everything collapsed together.

Regulators Who Didn’t Regulate

All of this happened in plain sight.

The complexity grew. The risks piled up.

And still—no one stepped in.

Regulators trusted the market to regulate itself. They believed in innovation, efficiency, and the wisdom of big finance.

When the system broke, they weren’t surprised.

They were simply unprepared.

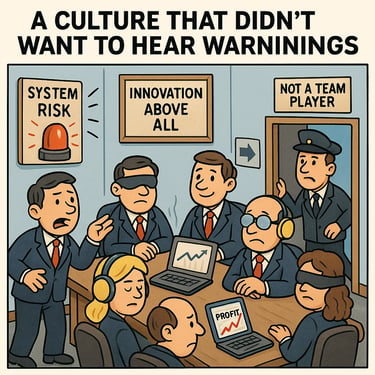

A Culture That Didn’t Want to Hear Warnings

As Tett reveals, it wasn’t just regulators who stayed quiet. Inside the banks, some people saw the danger and raised concerns. But questioning the system meant slowing it down. It meant being labeled as “anti-innovation” or simply “not a team player.”

The problem wasn’t ignorance—it was institutional silence.

Staying quiet was rewarded. Speaking up came with consequences. And so the machine rolled on.

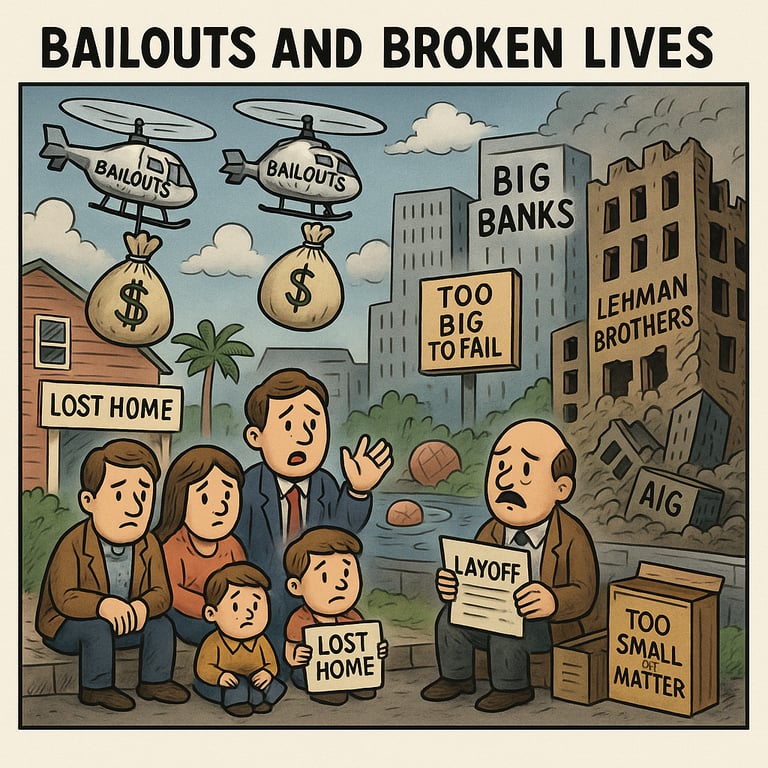

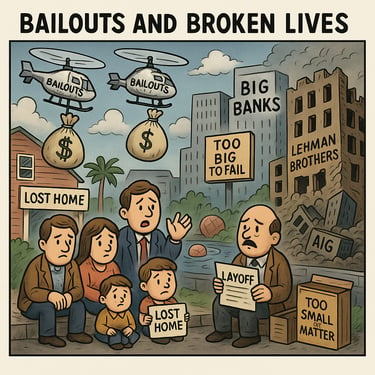

Bailouts and Broken Lives

When the crash came, it didn’t just hit banks. It hit everyone else.

People lost their jobs.

Families lost their homes.

Retirement savings disappeared.

Global economies stalled.

Meanwhile, governments rushed in—to bail out the banks.

AIG was rescued with billions.

Lehman Brothers was left to fall.

But the real cost was paid by people who never understood what went wrong—only that they were left behind.

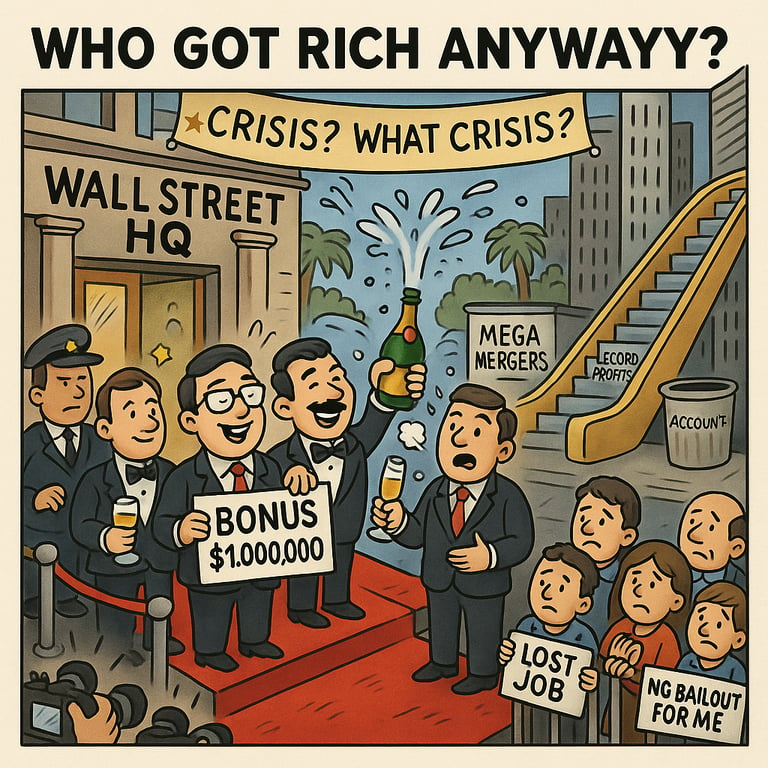

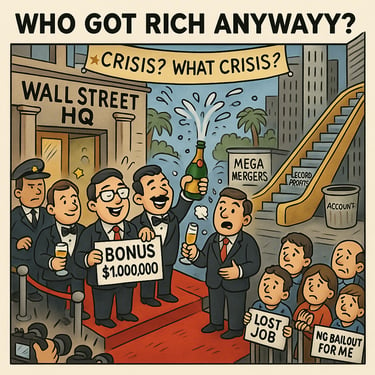

Who Got Rich Anyway?

While millions struggled, many investment banks walked away richer.

Bonuses kept flowing.

Mergers created even larger powerhouses.

Accountability? Nearly zero.

This wasn’t just a financial crash.

It was a redistribution of risk—and a privatization of profit.

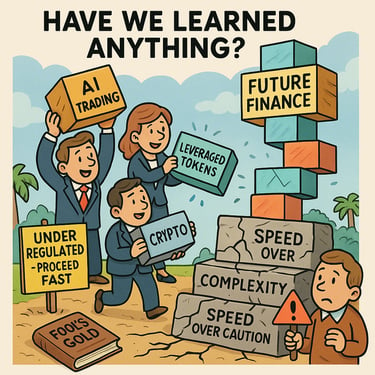

Have We Learned Anything?

Years later, the patterns are still with us.

Complex products no one fully understands.

New financial tools (crypto, AI trading, leveraged tokens) growing faster than regulation.

A system still built on speed, not reflection.

Fool’s Gold reads like a warning label for today.

Just because we’re not in a crisis now doesn't mean we’re not building one.

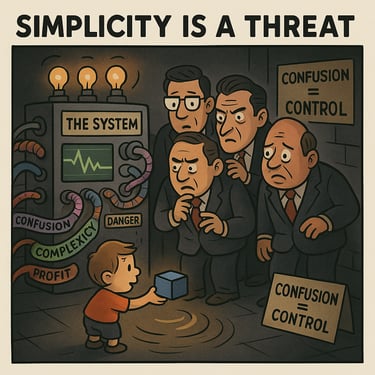

Final Thoughts – Simplicity Is a Threat

This book reminded me how fragile the financial system really is—and how much we need ethical decision-making if we want a future that’s stable, fair, and human.

Because even the smallest actions, made in the wrong hands, can ripple out into something much bigger than we imagine.

Confusion is profitable. And that’s exactly why simplicity is dangerous to the system.